What You Need To Know About Homeowner’s Insurance

Owning a home is a major milestone, but protecting it with the right homeowner’s insurance is just as important. Your home is likely one of your biggest investments, and having the right coverage ensures you’re prepared for the unexpected. Here’s what you need to know about homeowner’s insurance and how it can safeguard your property and financial well-being.

What Does Homeowner’s Insurance Cover?

A standard homeowner’s insurance policy typically includes several types of coverage:

-

Dwelling Coverage – This covers damage to your home’s structure from covered perils such as fire, windstorms, hail, and vandalism.

-

Personal Property Coverage – Protects your belongings, including furniture, electronics, and clothing, if they are damaged or stolen.

-

Liability Protection – Covers legal and medical expenses if someone is injured on your property or if you cause damage to someone else’s property.

-

Additional Living Expenses (ALE) – If your home becomes uninhabitable due to a covered loss, ALE helps pay for temporary housing and other necessary expenses.

What’s Not Covered?

While homeowner’s insurance provides extensive protection, some risks are not typically covered, including:

-

Flood damage (requires a separate flood insurance policy)

-

Earthquakes

-

Normal wear and tear

-

Pest infestations

It’s essential to review your policy and consider additional coverage if you live in areas prone to these risks.

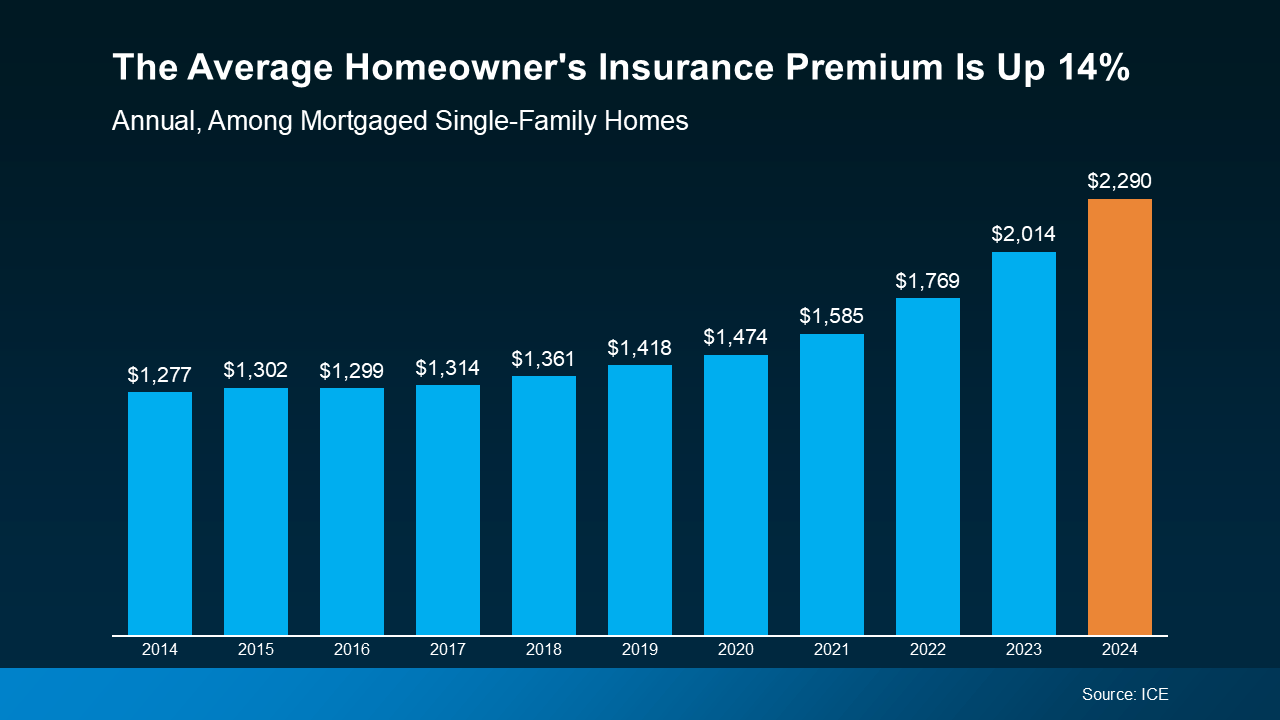

Basically, disasters are happening more often, repairs cost more, and insurers have to adjust their rates to keep up. Data from ICE Mortgage Technology helps paint the picture of how the average yearly premium has climbed over the last decade (see graph below):

How Much Coverage Do You Need?

To determine the right amount of coverage, consider:

-

Replacement Cost vs. Market Value – Insure your home for what it would cost to rebuild, not just its market value.

-

Personal Property Inventory – Take stock of your belongings to ensure you have enough coverage for your possessions.

-

Liability Limits – Make sure your policy provides adequate liability protection, especially if you have high-value assets.

Tips for Lowering Your Homeowner’s Insurance Premiums

-

Bundle Policies – Many insurance companies offer discounts when you bundle home and auto insurance.

-

Improve Home Security – Installing security systems, smoke detectors, and deadbolts can lower your premiums.

-

Raise Your Deductible – A higher deductible can lower your monthly premiums, but make sure you can afford the out-of-pocket cost in case of a claim.

-

Maintain Good Credit – Some insurers use credit scores to determine rates, so maintaining good credit can help reduce costs.

Final Thoughts

Homeowner’s insurance is essential for protecting your home and financial future. By understanding your policy, assessing your coverage needs, and exploring ways to save, you can ensure you have the right protection in place.

If you have any questions or need help finding the right policy, reach out to a trusted insurance professional to guide you through the process!

Book your appointment and let’s talk to take the next step in your real estate journey. Schedule a real estate consultation with one of our team members.

Categories

- All Blogs (154)

- Agent (146)

- Baltimore (136)

- Baltimore Real Estate (133)

- Buying (127)

- Closing Cost (48)

- Commercial Real Estate (132)

- D.C (131)

- Downsizing (122)

- Equity (145)

- First time homebuying (119)

- home buying tips (123)

- Home Selling (94)

- home selling tips (55)

- Homebuying (123)

- Investing (138)

- Lower Prices (142)

- Market Reports (120)

- Market Update (122)

- Maryland (140)

- Maryland Real Estate (140)

- mortgage (119)

- mortgage rates (122)

- Property Taxes (25)

- purchasing a home (124)

- Real Estate (148)

- Real Estate Agent (148)

- Real Estate Report (113)

- Retirement (103)

- Selling (97)

- VA Loan (16)

- Veterans (14)

- Washington D.C (121)

Recent Posts