The #1 Reason Buyers Walk Away (And How To Get Ahead of It)

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

The Top Dealbreaker: Issues That Pop Up During the Inspection

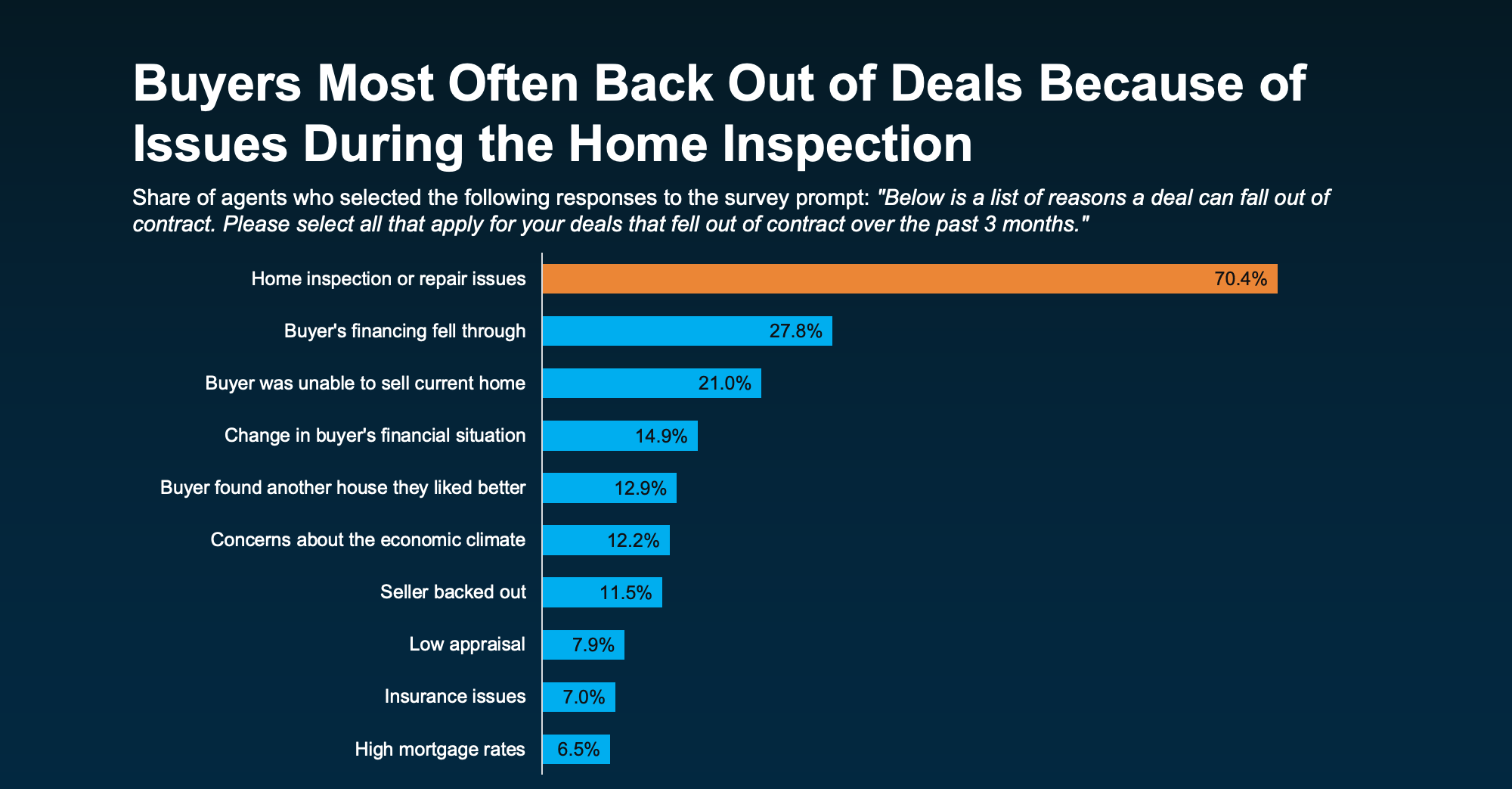

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

The Biggest Reason Buyers Walk Away

While there are multiple factors that can derail a deal, one stands out above the rest: financing issues.

Even the most motivated buyers can fall out of a deal if they struggle to secure a mortgage or run into unexpected financial hurdles. Sometimes it’s a credit snag, a last-minute debt discovery, or simply underestimating the costs involved in purchasing a home. Whatever the cause, financing problems are the number-one reason transactions fail.

How to Get Ahead of It

The good news? Most financing hurdles are preventable with the right preparation and proactive steps:

-

Pre-Approval is a Must

Encourage buyers to get pre-approved before they start house hunting. Pre-approval not only sets realistic expectations but also strengthens their position when making an offer. -

Full Transparency on Finances

Buyers should provide all relevant financial information upfront. Hidden debts, recent large purchases, or unreported income issues can be flagged early and addressed before they derail the sale. -

Work with Experienced Lenders

A knowledgeable lender can foresee potential snags and guide buyers through them before they become deal-breakers. -

Plan for Extra Costs

Closing costs, inspections, and unexpected repairs can surprise first-time buyers. Educate them on budgeting for these expenses so there are no last-minute shocks. -

Regular Communication

Keeping lines of communication open throughout the process ensures that small issues are addressed promptly, preventing them from snowballing into deal-ending problems.

The Bottom Line

Understanding why buyers walk away allows you to take action before it’s too late. By focusing on pre-approval, transparency, and proactive planning, you can dramatically reduce the risk of losing a sale. In real estate, preparation isn’t just helpful—it’s the difference between a closed deal and a missed opportunity.

Book your appointment and let’s talk to take the next step in your real estate journey. Schedule a real estate consultation with one of our team members.

Categories

- All Blogs (154)

- Agent (146)

- Baltimore (136)

- Baltimore Real Estate (133)

- Buying (127)

- Closing Cost (48)

- Commercial Real Estate (132)

- D.C (131)

- Downsizing (122)

- Equity (145)

- First time homebuying (119)

- home buying tips (123)

- Home Selling (94)

- home selling tips (55)

- Homebuying (123)

- Investing (138)

- Lower Prices (142)

- Market Reports (120)

- Market Update (122)

- Maryland (140)

- Maryland Real Estate (140)

- mortgage (119)

- mortgage rates (122)

- Property Taxes (25)

- purchasing a home (124)

- Real Estate (148)

- Real Estate Agent (148)

- Real Estate Report (113)

- Retirement (103)

- Selling (97)

- VA Loan (16)

- Veterans (14)

- Washington D.C (121)

Recent Posts