Rent or Buy? The Real Tradeoff Most People Don’t Talk About

For years, the rent vs. buy debate has been framed as a simple financial equation: renting is “throwing money away,” while buying is “building equity.” But that narrative misses a much deeper—and often more important—tradeoff that most people don’t talk about.

It’s not just about money. It’s about flexibility vs. control.

The Hidden Tradeoff

When you rent, you’re paying for flexibility.

You can move when your job changes, when your lifestyle shifts, or when you simply want something new. There’s no long-term commitment, no property taxes, no surprise repair bills. Your landlord carries the risk—you carry the freedom.

When you buy, you’re paying for control.

You own the space. You can renovate, customize, and create long-term stability. Over time, you may build equity and benefit from appreciation. But that control comes with responsibility—and less mobility.

How Homeownership Builds Your Wealth Over Time

On the other hand, owning a home is one of the most consistent ways people build wealth over time. Why? When you’re a homeowner, you gain something called equity. That’s the difference between what your home is worth and what you owe.

That equity grows with every monthly payment you make. It also gets a boost as home values go up through the years – and it adds up quicker than you may think.

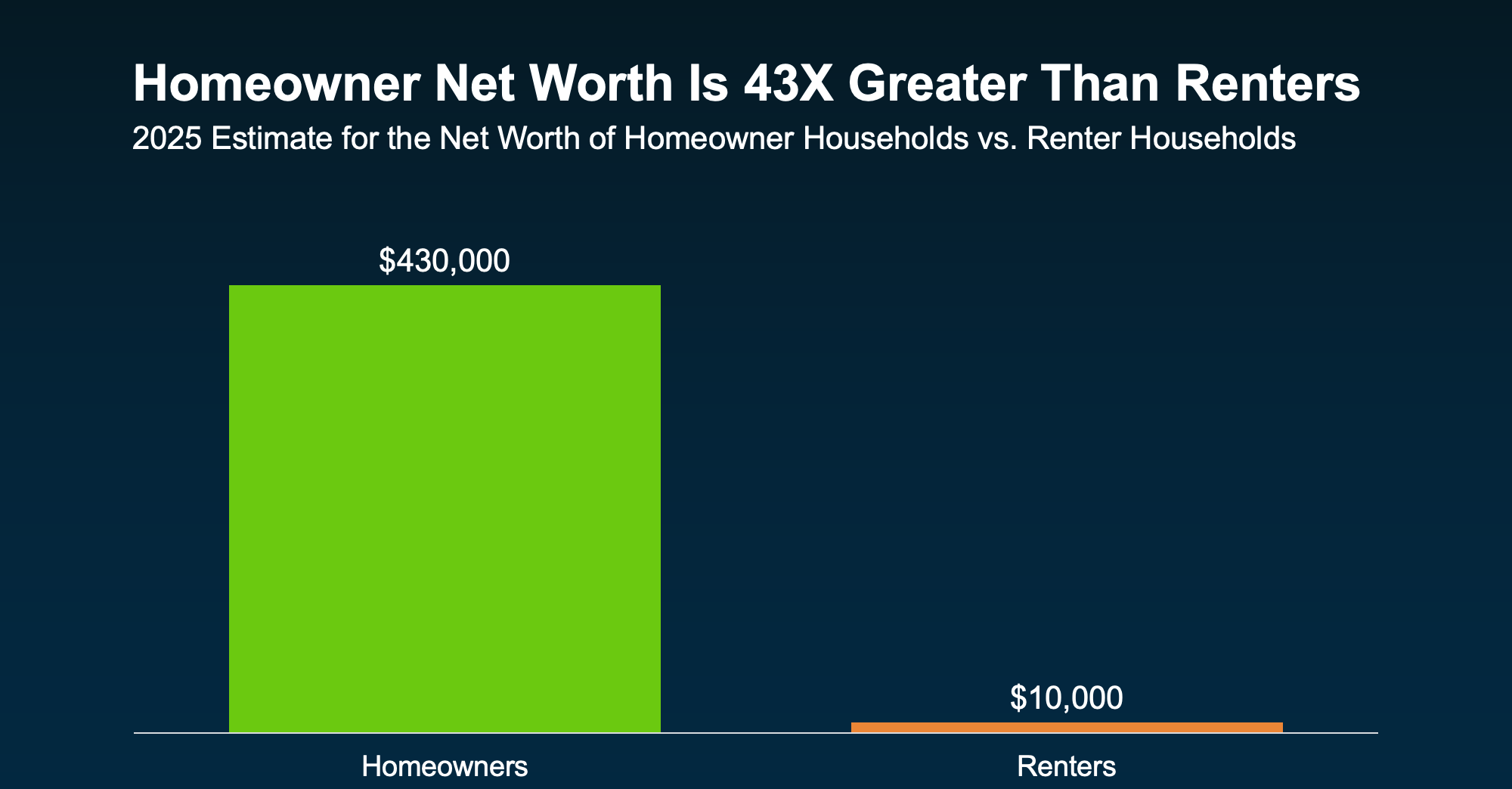

Today, the National Association of Realtors (NAR) says the average homeowner’s net worth is 43X greater than that of a renter:

The dollars in the visual don’t lie. On average, here’s how net worth compares:

- Homeowners: $430k

- Renters: $10k

And it’s not because homeowners make wildly different decisions day to day. It’s because over time, one path builds something, and the other doesn’t.

So sure, buying comes with some upfront costs and more responsibility. But it’s basically a savings account you can live in.

The Financial Reality (That’s Often Oversimplified)

Yes, homeowners build equity—but it’s not as straightforward as it sounds.

Owning a home includes:

- Mortgage interest

- Property taxes

- Maintenance and repairs

- Insurance

- Opportunity cost of your down payment

Renting, on the other hand, offers predictability and frees up capital that could be invested elsewhere.

In some markets, renting and investing the difference can actually outperform buying—especially in the short to medium term.

Time Horizon Changes Everything

One of the biggest factors in this decision is how long you plan to stay.

- Short-term (1–3 years): Renting usually makes more sense due to transaction costs and market risk.

- Mid-term (3–7 years): It depends on the market, appreciation, and your financial discipline.

- Long-term (7+ years): Buying often becomes more advantageous as equity builds and costs stabilize.

Lifestyle Matters More Than You Think

This decision isn’t just financial—it’s personal.

Ask yourself:

- Do you value mobility or stability?

- Are you ready for the responsibilities of ownership?

- Do you want to customize your living space?

- Is your income stable enough to handle unexpected costs?

There’s no universal “right” answer—only what aligns with your current stage of life.

The Real Question You Should Be Asking

Instead of asking, “Is renting a waste of money?”, ask:

“What am I paying for—flexibility or control—and which one matters more to me right now?”

Because at the end of the day, both renting and buying have value. The key is understanding which tradeoff you’re willing to make.

Final Thought

The smartest decision isn’t always the one that looks best on paper—it’s the one that fits your life. And sometimes, the freedom of renting or the stability of owning is worth more than any spreadsheet can show.

Book your appointment and let’s talk to take the next step in your real estate journey. Schedule a real estate consultation with one of our team members.

Categories

- All Blogs (154)

- Agent (146)

- Baltimore (136)

- Baltimore Real Estate (133)

- Buying (127)

- Closing Cost (48)

- Commercial Real Estate (132)

- D.C (131)

- Downsizing (122)

- Equity (145)

- First time homebuying (119)

- home buying tips (123)

- Home Selling (94)

- home selling tips (55)

- Homebuying (123)

- Investing (138)

- Lower Prices (142)

- Market Reports (120)

- Market Update (122)

- Maryland (140)

- Maryland Real Estate (140)

- mortgage (119)

- mortgage rates (122)

- Property Taxes (25)

- purchasing a home (124)

- Real Estate (148)

- Real Estate Agent (148)

- Real Estate Report (113)

- Retirement (103)

- Selling (97)

- VA Loan (16)

- Veterans (14)

- Washington D.C (121)

Recent Posts