One Key Sign We’re Not Headed for a Wave of Foreclosures

If you’ve been following real estate headlines, you’ve probably seen concerns about a potential surge in foreclosures. It’s a fair question—especially with higher interest rates and affordability challenges. But when we look closely at the data, there’s one key sign that strongly suggests we’re not heading toward a foreclosure crisis:

Homeowners Have Record Levels of Equity

Unlike the conditions leading up to the 2008 Financial Crisis, today’s homeowners are sitting on significant equity in their homes—and that changes everything.

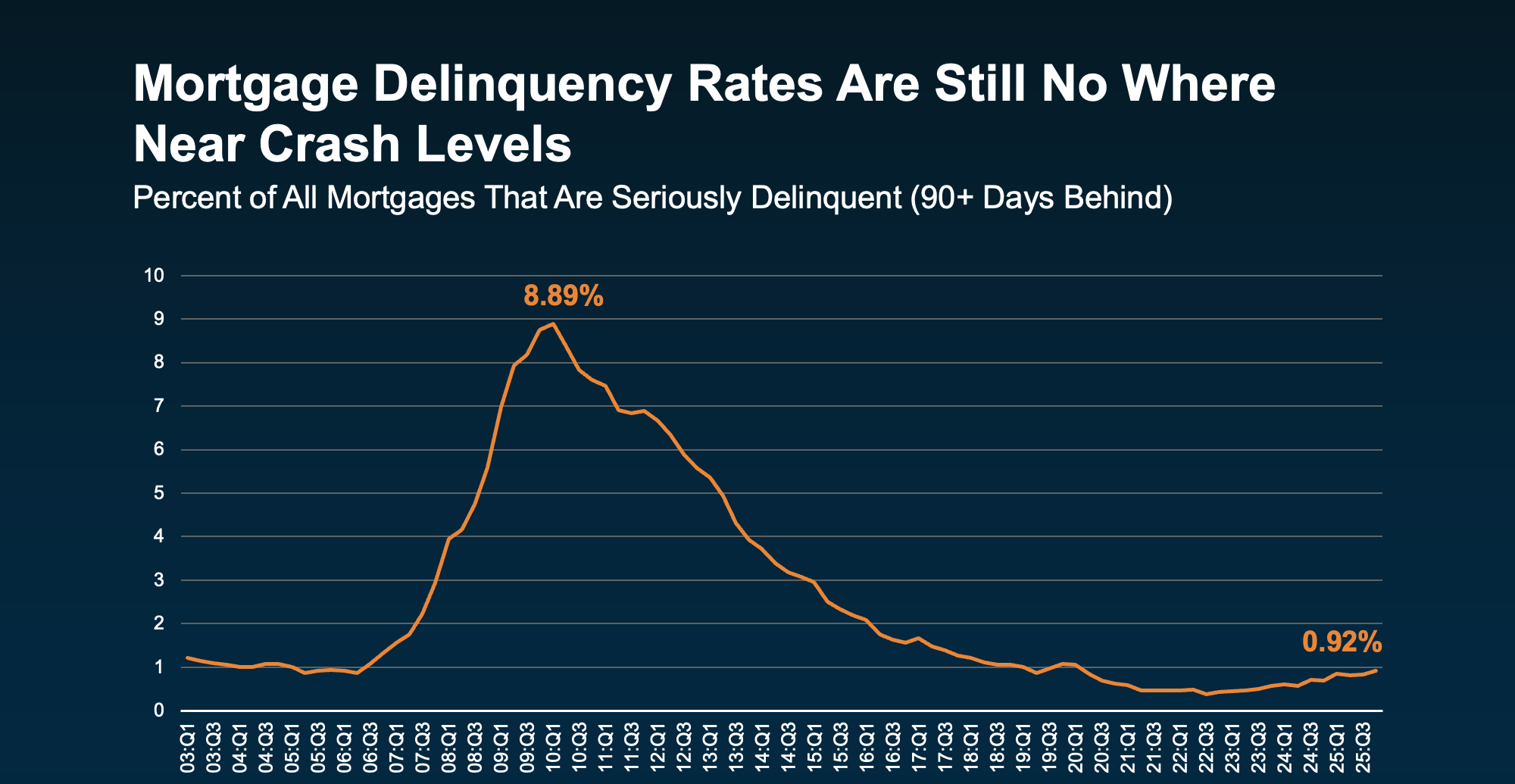

While those have increased slightly, data from the New York Fed shows they still remain low. And they aren’t anywhere close to levels seen when the market crashed (see graph below):

Why Equity Matters

Equity is the difference between what a homeowner owes on their mortgage and what their home is worth. Over the past several years, home prices have risen substantially, allowing homeowners to build strong equity positions.

This means:

-

Homeowners are less likely to default on their loans

-

Even if they face financial hardship, they can sell their home instead of going into foreclosure

-

Many have a financial cushion they didn’t have in the past

Then vs. Now

During the housing crash of 2008, many homeowners had little to no equity—or worse, they owed more than their homes were worth. This led to a wave of foreclosures because selling wasn’t a viable option.

Today’s market is very different:

-

Lending standards are much stricter

-

Most homeowners have fixed-rate mortgages at lower interest rates

-

There’s no widespread overleveraging like before

What This Means for the Market

While foreclosure activity may increase slightly from historically low levels (which is normal as markets stabilize), a massive spike is unlikely. The strong equity position of homeowners acts as a safeguard, preventing the kind of widespread distress seen in the past.

When households feel financial pressure, they tend to prioritize their mortgage payment above almost everything else. Because the last thing they want to lose is their home.

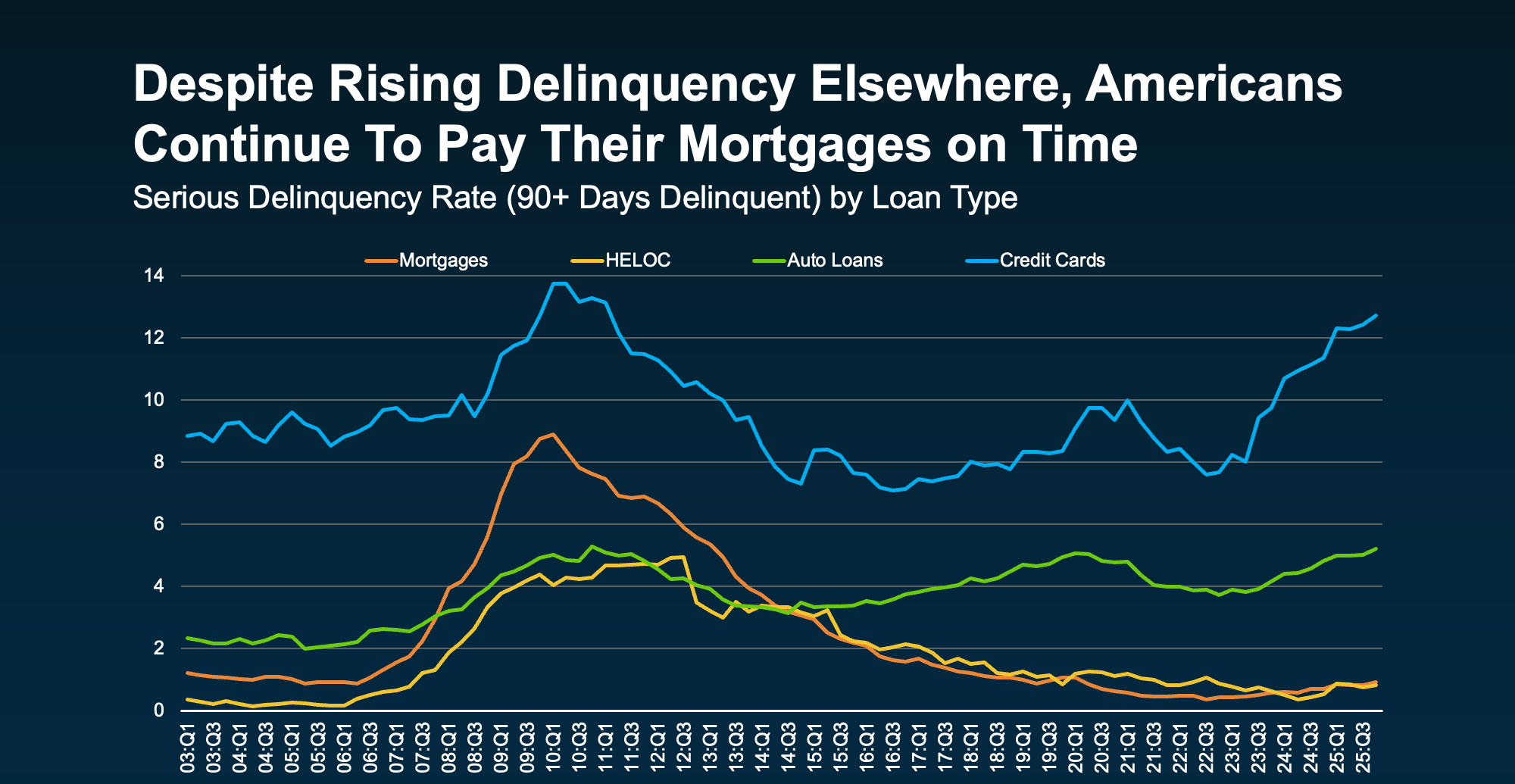

Data from the New York Fed shows serious delinquencies have risen more for credit cards and auto loans (the blue and green lines). But mortgage delinquencies and home equity lines of credit (borrowing against the value of your home) aren’t seeing the same big uptick (the yellow and orange lines). They’re a lot more stable overall.

The Bottom Line

The housing market isn’t without its challenges—but the foundation is far stronger than it was in previous downturns. Thanks to record-high homeowner equity, the risk of a large-scale foreclosure wave remains low.

Book your appointment and let’s talk to take the next step in your real estate journey. Schedule a real estate consultation with one of our team members.

Categories

- All Blogs (153)

- Agent (145)

- Baltimore (135)

- Baltimore Real Estate (132)

- Buying (126)

- Closing Cost (47)

- Commercial Real Estate (131)

- D.C (130)

- Downsizing (122)

- Equity (144)

- First time homebuying (118)

- home buying tips (122)

- Home Selling (94)

- home selling tips (55)

- Homebuying (122)

- Investing (137)

- Lower Prices (141)

- Market Reports (119)

- Market Update (121)

- Maryland (139)

- Maryland Real Estate (139)

- mortgage (119)

- mortgage rates (122)

- Property Taxes (25)

- purchasing a home (124)

- Real Estate (147)

- Real Estate Agent (147)

- Real Estate Report (112)

- Retirement (103)

- Selling (97)

- VA Loan (16)

- Veterans (14)

- Washington D.C (120)

Recent Posts