How Your Equity Could Help Younger Generations Buy a Home

Owning a home is a dream that seems increasingly out of reach for many younger generations. Skyrocketing home prices, rising interest rates, and tighter lending requirements make it challenging for first-time buyers to get a foothold in the housing market. But did you know that the equity you’ve built in your home could be a powerful tool to help younger generations achieve their dream of homeownership?

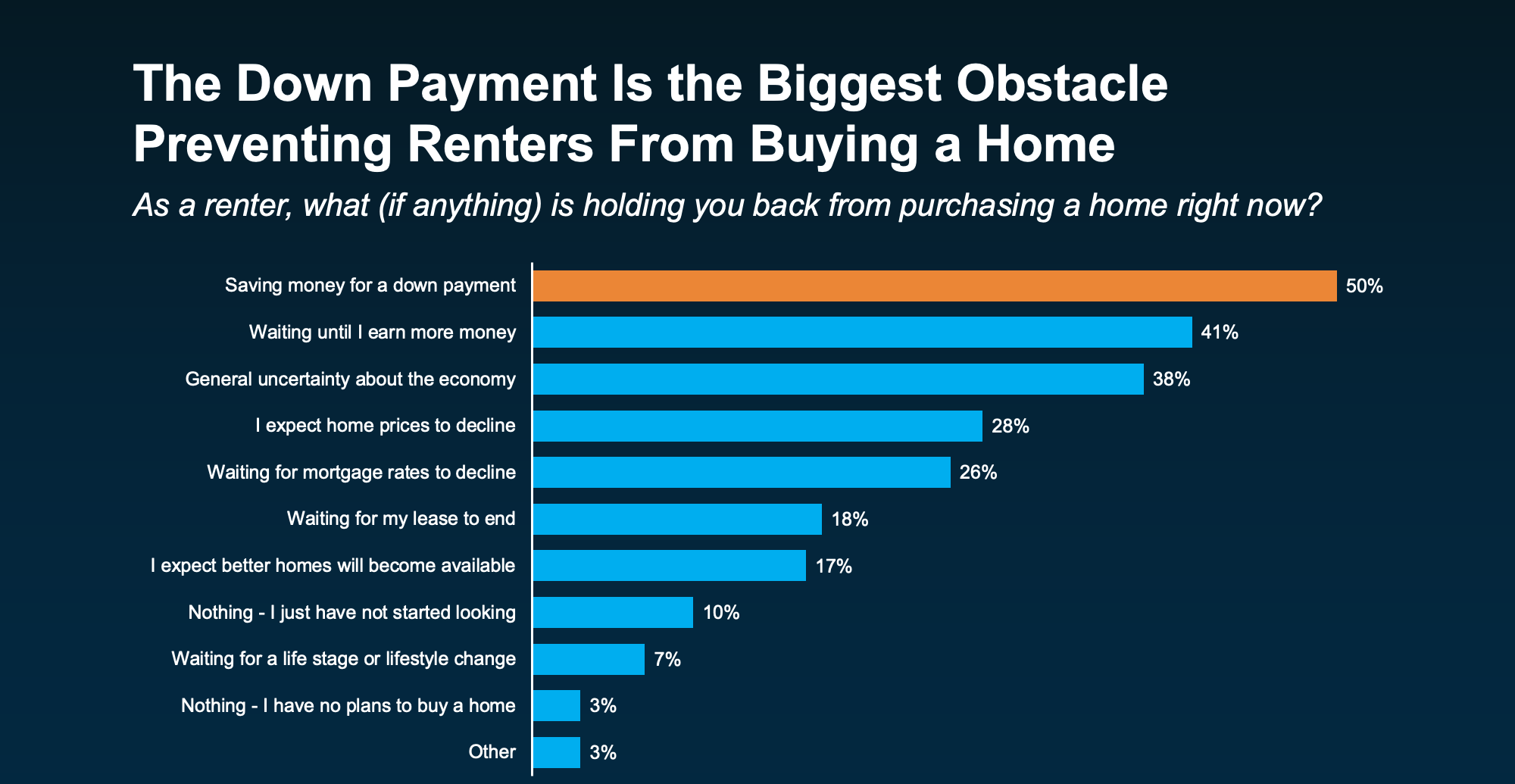

The #1 Thing Holding Young Buyers Back

When John Burns Research & Consulting (JBREC) asked renters what’s keeping them from buying, the top answer wasn’t mortgage rates or home prices. It was the upfront cost, particularly saving enough for their down payment (see graph below):

Understanding Home Equity

Home equity is the portion of your home that you truly “own.” It’s the difference between your home’s current market value and the amount you still owe on your mortgage. For example, if your home is valued at $400,000 and your mortgage balance is $250,000, you have $150,000 in equity. Over time, as your mortgage balance decreases and property values rise, your equity grows—a financial resource that can be tapped in a variety of ways.

Ways Your Equity Can Help Younger Buyers

-

Gifting a Down Payment

One of the most direct ways to assist is by gifting a portion of your home equity to a child, grandchild, or close relative. Even a modest gift can help them cover a down payment, potentially unlocking lower interest rates and avoiding costly mortgage insurance. -

Co-Buying a Home

You can use your equity to co-invest in a property with a younger buyer. This partnership allows them to purchase a home sooner while you maintain ownership interest. It can also be structured so that your share grows as the property appreciates, benefiting both parties financially. -

Home Equity Loan or Line of Credit (HELOC)

If you prefer not to gift equity outright, a home equity loan or line of credit can provide funds for a younger buyer’s down payment. The loan can be repaid over time, offering flexibility while still helping them get into a home. -

Financing Renovations or Improvements

If the younger generation buys a fixer-upper, your equity could help finance the renovations needed to make the home livable. This approach can be a win-win: they get a move-in-ready home, and the property value increases over time.

The Benefits Go Both Ways

Helping younger family members or friends with homeownership isn’t just altruistic—it can be financially strategic as well. By assisting them now, you may help them build wealth earlier, which strengthens family financial stability overall. Additionally, co-investing or gifting in smart ways can have tax benefits when planned properly with a financial advisor.

Things to Keep in Mind

While using your home equity to assist others can be rewarding, it’s important to consider:

-

Your Financial Security – Ensure that helping someone else doesn’t put your retirement or long-term plans at risk.

-

Loan Terms and Interest Rates – If using a HELOC or co-buying, make sure terms are manageable and clearly understood.

-

Professional Advice – Consult a financial advisor or real estate professional to navigate legal and tax implications.

Final Thoughts

Your home equity represents years of hard work and smart financial decisions. By thoughtfully leveraging it, you can help younger generations take their first step into homeownership—creating opportunities and memories that last a lifetime. Homeownership isn’t just about property—it’s about building a legacy.

Book your appointment and let’s talk to take the next step in your real estate journey. Schedule a real estate consultation with one of our team members.

Categories

- All Blogs (153)

- Agent (145)

- Baltimore (135)

- Baltimore Real Estate (132)

- Buying (126)

- Closing Cost (47)

- Commercial Real Estate (131)

- D.C (130)

- Downsizing (122)

- Equity (144)

- First time homebuying (118)

- home buying tips (122)

- Home Selling (94)

- home selling tips (55)

- Homebuying (122)

- Investing (137)

- Lower Prices (141)

- Market Reports (119)

- Market Update (121)

- Maryland (139)

- Maryland Real Estate (139)

- mortgage (119)

- mortgage rates (122)

- Property Taxes (25)

- purchasing a home (124)

- Real Estate (147)

- Real Estate Agent (147)

- Real Estate Report (112)

- Retirement (103)

- Selling (97)

- VA Loan (16)

- Veterans (14)

- Washington D.C (120)

Recent Posts